PEG’s Quarter 1 Economic Update

Hello PEG Members!

Welcome to the 2026 Q1 Economic Outlook from PEG. I hope everyone has had a great start to the year. I am very excited to see many of our members at the ARA show at the end of the month.

Our sources at ITR Economics, Dodge Construction, Rouse Analytics, and our own data show that we are currently in a prosperous spot in the macroeconomy. Consumer and B2B spending are in growth phases, the labor market continues to strengthen, adjustments to tariffs are settling, and industrial production is in growth.

- ITR, The Core US Economy at-a-Glance, February 2026

This spells great news for the country as a whole; however, when looking at construction, the industry is shown to be facing some serious headwinds.

“Leading indicators tell us that the year ahead will be one of growth, but it will be at a relatively mild to moderate pace.

The construction segments of GDP are the outliers. Nonresidential structures (3/12 is -5.9%) lag the macroeconomy; the current decline reflects the prior jump in interest rates and prior sluggish economic growth. Investments in residential structures and equipment are down 2.3% from one year ago.” – ITR, Residential Construction a soft spot in a growing economy

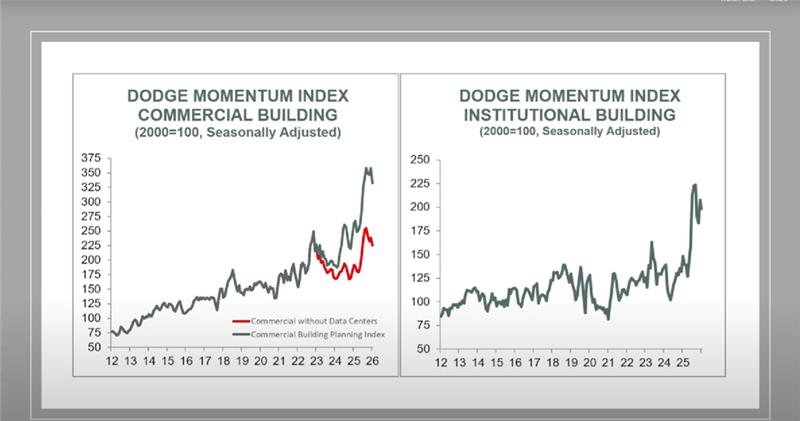

Dodge Construction’s reports mirror these findings. The Dodge Momentum Index (DMI) lowered 6% in January due to lowered activity in commercial and institutional planning.

Dodge found that this was a normalization from heightened activity towards the end of 2025.

- Dodge Construction, Dodge Momentum Index down 6% in January

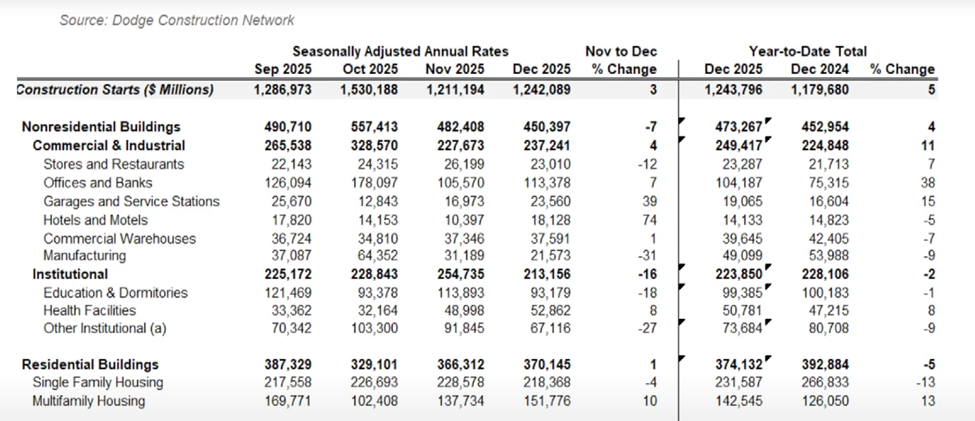

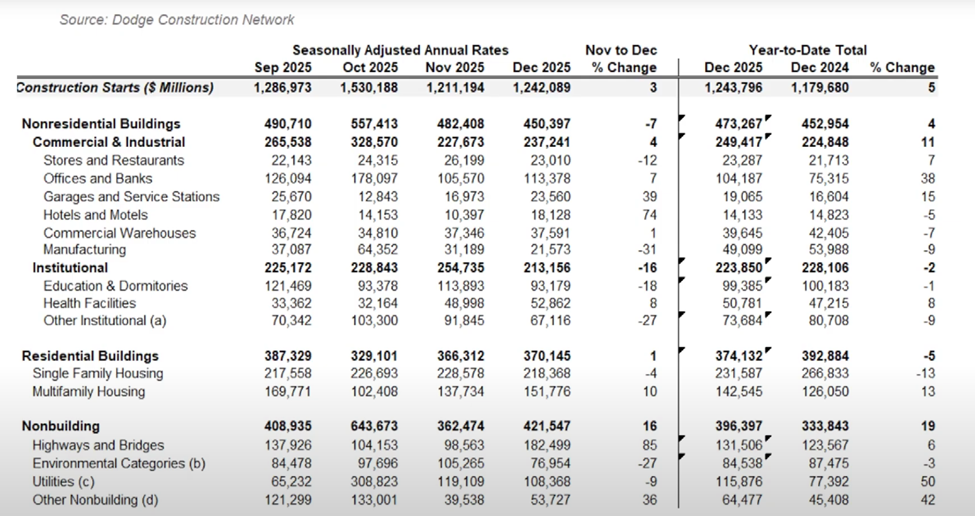

Fortunately, this increased planning activity towards the end of ’25 spells good news for starts, which increased 3% in December ’25. In starts, we find that non-residential and non-building construction led the way, with 5% and 19% year-over-year growth rates, respectively.

- Dodge Construction, Construction Starts Grow 3% in December

With both good news and bad news ahead of us, this report will focus on the changes in the current construction markets, supply for equipment, current equipment value reports, the labor market, and management strategies for Q2 and beyond in 2026.

Demand: Single-unit housing continues to struggle, Multi-unit steps up to take its place

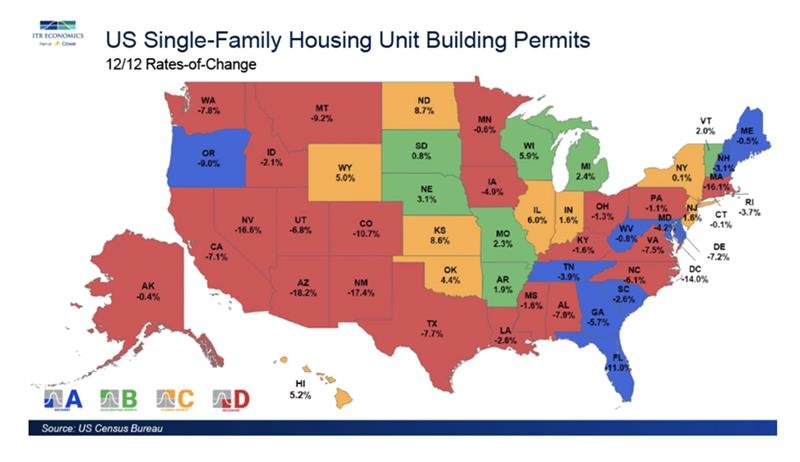

ITR is forecasting decline in US Single-Unit Starts in 2026, a relatively flat 2027, and then rise in 2028. Unfortunately, this spells less site activity in 2026. With strong consumer wallets and existing home sales selling at a rate 4 times higher than new builds, there is still a strong market for home services, renovations, and maintenance, so look to support your customers in those industries.

ITR has noticed that the hottest housing markets are generally mid-size cities, largely in the Midwest and Northeast, with relatively more affordable home prices. Luxury homes are taking longer to sell and have come down in price. Affordability is hot, luxury is not.

ITR, Residential Construction a soft spot in a growing economy

With interest rates maintaining their stickiness and consumers still living off of the “golden handcuffs” of lower mortgage rates from years prior, affordability continues to be one of the main constraints for potential buyers. This has continued to draw consumers and builders to multi-unit starts. ITR and Dodge do not see this trend changing anytime soon.

- Dodge Construction, Construction starts Grow 3% in December

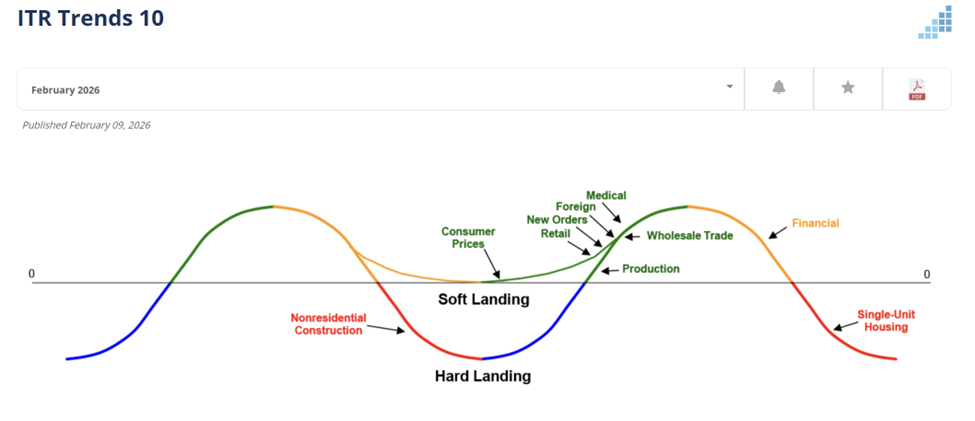

Notice here how single family and multifamily housing year over year growth rates have offset each other. Overall, the residential market is often seen as a leading indicator for the economy, and it continues to be in a recession. Here is the trends report from ITR:

- ITR Trends 10, February 2026

Fortunately, we see that non-residential construction is nearing a recovery period, following the current growth periods of production, medical, retail, consumers, and new orders.

Demand: Commercial and non-building construction maintain growth

- Dodge Construction, Construction starts grow 3% in December

Looking at the other sections of this chart, Commercial and Industrial construction starts saw an 11% year over year growth from Dec 2024 to Dec 2025, with Offices and Banks, Garages and Service stations, and hotels leading the way. Institutional construction did not have much change aside from an 8% year over year growth within Health Facilities. Lastly, utilities saw major growth (according to Dodge, this was mainly due to Data Center activity) and highways and bridge starts saw major growth moving into 2026.

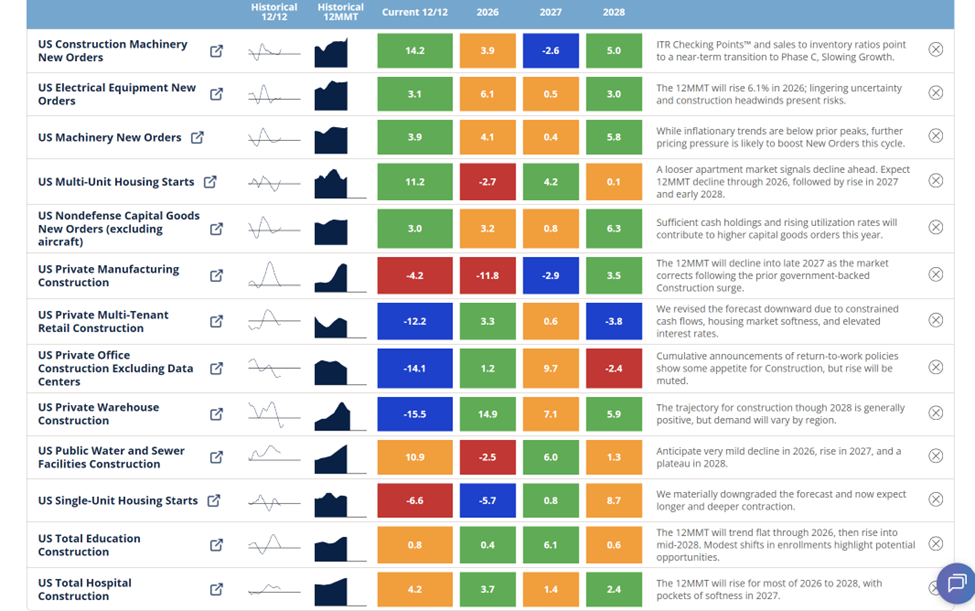

- ITR, Construction Economy at-a-Glance, February 2026

ITR’s dashboard mirrors these sentiments, with most non-residential and non-building sectors in slowing growth or recovery. As stated prior, fortunately, these sectors follow the current growth of construction machinery new orders, capital goods orders, and overall industrial prosperity.

Supply: An economy in growth mode

Fortunately, the supply end of the machinery industry is looking much more promising.

As ITR reports, Construction Machinery New Orders and Capital Goods New Orders are in growth modes, nearing slowing growth. This shows that there is currently a great demand for construction machinery. For rental operations, this will make it a strong time to resell used equipment and look for greater utilization rates within your fleets. For dealerships, take note of high demand in your pricing decisions. Do beware of the slowing growth around the corner. Make sure not to overexpand during this time.

Rouse’s report mirrors these findings, with the Fair Market Value (FMV) remaining flat in most equipment. The pieces of equipment closest to their July ’24 values were Truck Tractors, Forklifts, Excavators, Wheel Loaders, and Aerial lifts. (Rouse, The Equipment Report, December 2025)

With B2B and consumer spending seen in growth modes, take advantage of the spending that will occur this year.

Labor Market: Employment projected to grow through 2028

ITR suggests employment will continue to grow through 2028, with a slight shift downward after. Although the balance of power shifted towards the employers last year, the labor market is likely to become more competitive soon as the macroeconomy ramps up. With increased spending around, beware of increasing wages, more negotiations, and a tighter market.

The Year Ahead:

With the current market, look to take advantage of the B2B and Consumer spending, while remaining focused on the portions of the construction industry that you serve.

For those focused on…

Homeowners: expect more spending due to increased disposable income.

Contractors that build new homes; beware of the contraction that the single-unit residential industry is currently going through.

Contractors that service homes; expect greater household spending.

Contractors building commercial and retail projects; expect activity from those supporting parking garages, offices, hospitals, and utilities work.

Contractors looking to own construction equipment; know that demand is currently at a high.

Despite the optimism of the market, the construction industry continues to face headwinds so hang in there. See you in the next installment of the Economic Update.

If you would like any further analysis feel free to reach out to Dan (dcrowley@peerexecutivegroups.com), Charlie (cpetersen@peerexecutivegroups.com), or I (ncrowley@peerexecutivegroups.com) for more information.