Quarter 2 Economic Update

Hello Peer Executive Group Members!

Welcome to the 2026 Q2 Equipment Economic Outlook from PEG. Our sources at ITR Economics, Dodge Construction, and our own data have proven very optimistic for the current state of the construction and machinery industries, and macroeconomy. There have been recent shocks felt due to the war in Iran, but growth is still accelerating in many areas of the economy.

Before we dive deep into the economy at large, I want to highlight some statistics from our 2025 Year-End Composite Book for Equipment:

As you all know, Charlie has been working hard on developing the books this spring for our Event and Equipment groups, and he has finally solidified the book for Equipment. With 67 submissions, we found that the:

PEG Member Median for Total Revenue was: $5.6 million

Rental Revenue was: $4.5 million

EBITDA was: 25%

Dollar Utilization was: 51%

Labor Cost as % of Revenue was: 32%

Return on Assets was:22%

This is just a snapshot, but if you would like to dive deeper into the composite book, feel free to reach out to Dan (dcrowley@peerexecutivegroups.com) or Charlie (cpetersen@peerexecutivegroups.com)!

In addition, through our collection of ROC information, we have found that the PEG average 12/12 growth rate for Equipment Operators through March 2026 is 17% amongst 42 operations. This is purely top-line rental revenue, so do beware that younger businesses and businesses going through acquisitions can skew these numbers.

Event folks – tune back in next quarter for your results!

This growth rate for our members is reflected in much of what ITR and Dodge Construction had to share at the beginning of Q2.

- ITR, The Core US Economy at-a-Glance, May 2026

As stated before, the economy is continuing to show promising signs of growth in many areas. Due to the War in Iran, there has been a cooling down of some sectors, specifically private sector employment and consumer spending, but nondefense capital goods new orders, industrial production, and GDP continue to grow.

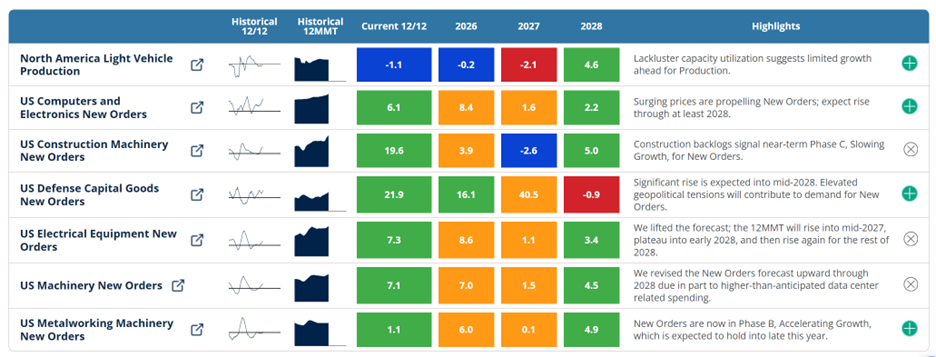

Moving to construction, the industry continues to be dominated by data center projects. The tech boom is rife with opportunity, and ITR quotes a great adage here, “During a gold rush, sell shovels.” This boom is not new to anyone at this point, but is reflected in these numbers:

Construction Machinery 12/12 of 19.6%

HVAC Equipment 12/12 of 14.5%

Electrical Equipment New Orders 12/12 of 7.3%

Turbines, Generators, and Power Transmission Equipment 12/12 of 6.0%

In addition to construction of warehouses, utilities and electrical construction have also seen great growth due to these projects. ITR states to take advantage of this trend, but to remain cautious of adding overhead tied to the boom.

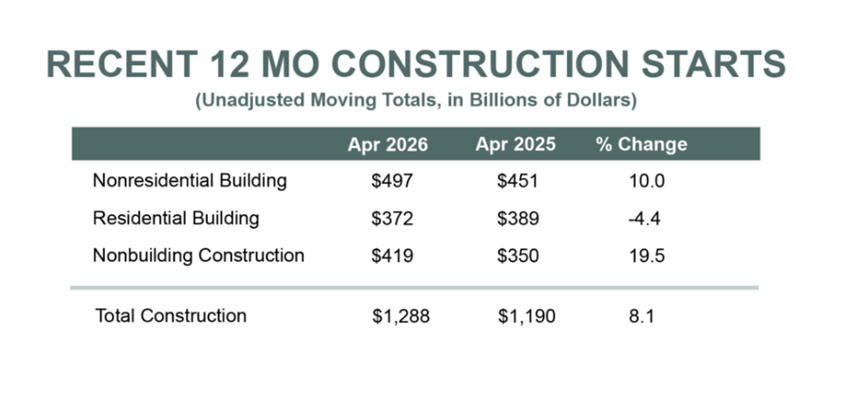

- Dodge Construction, Construction Starts Power On, Up 9% in April

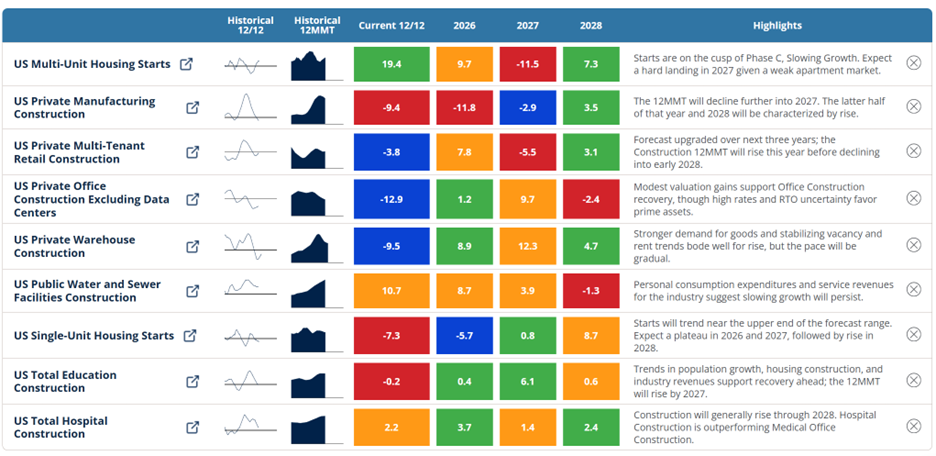

Both Dodge and ITR find that residential construction continues to be a sore spot in the industry, with a 12/12 growth rate of -4.4%. Amongst residential, single-unit construction tends to be recovering from a low (increased 4.2% month/month, down 15.0% year/year), whilst multi-unit is cooling down after growth for the past year (down 7.2% m/m, up 17.4% y/y)

Moving to non-residential, on a 12/12 basis, starts are up 10.0%. Commercial and industrial construction starts are up 30.4% year-to-date, whereas institutional starts are down 12.1% year-to-date. The hottest commercial project types (aside from data centers) were found in parking garages, warehouses, and stores. Institutional projects saw month/month growth in education and healthcare.

Non-building construction has grown 19.5% on a 12/12 basis, with the hottest month/month growth in miscellaneous nonbuilding, highways and bridges, and environmental public works. Electric power/utilities are cooling down but remain bolstered by large natural gas facilities and renewable projects.

Regionally, total construction starts in April rose in the Midwest (+66.9% month/month), the Northeast (+19.9% m/m), and the South Atlantic (+9.3% m/m). Meanwhile, the South Central (-14.5% m/m), and the West (-8.6% m/m) saw declines.

- ITR, The US Construction Economy at-a-Glance, May 2026

Supply: Continued growth, but with a slowdown approaching

Moving to the supply side, industrial production continues to look promising.

- ITR, The US Manufacturing Economy at-a-Glance, May 2026

As stated before, we see that US Construction Machinery New Orders are currently at 19.6% 12/12 growth. Although this will be cooling in the next couple of years, it continues to show that demand is currently very strong for equipment. For rental operations, this will make it a strong time to resell used equipment and look for greater utilization rates within your fleets. For dealerships, take note of high demand in your pricing decisions.

Labor Market: Employment slows, but expected to pick up towards the end of the year

ITR reports that, “US Private Sector Employment in the 12 months through April averaged 135.1 million workers, 0.4% above the same period one year ago. We expect Employment will generally rise through at least 2028.” In addition, ITR finds that layoffs are occurring at normal levels. This, in addition to rising industrial demand and stability in US Retail Sales, bodes well for the market with ITR predicting a “moderate hire, low fire” environment later this year.

The Year Ahead:

We have all certainly felt the shocks on fuel pricing in recent months. ITR predicts that this pricing will drop back in price as the War in Iran moves closer to a resolution.

-ITR

Despite this shock, the economy continues to grow in consumer spending, industrial production, manufacturing, and non-residential and non-building construction. Expect continued growth in those areas of your market tied to commercial construction, multi-unit housing, non-building construction (especially utilities), and educational and healthcare institutional construction.

Hope everyone has a great summer, and as always, feel free to reach out with any questions, my email is ncrowley@peerexecutivegroups.com.